The form will specify the items being ordered, the quantity, price, and terms. One copy is sent to the vendor (supplier) of the goods, and one copy is sent to the accounts payable department to be later compared to the receiving ticket and invoice from the vendor. The $1,500 balance in Wages Payable is the true amount not yet paid to employees for their work through December 31.

Closing Entries

It is simply a reclassification that happens as the financial statements are being prepared (often on the worksheet). Since Unearned Revenues is a balance sheet account, its balance at the end of the accounting year will carry over to the next accounting year. On the other hand Service Revenues is an income statement account and its balance will be closed when the current year is over. Interest payable on a loan refers to the periodic interest payments that are required to be made by the borrower to the lender under the terms of the loan agreement. The interest rate is typically stated as a percentage of the outstanding principal balance and is paid over the life of the loan. Interest payments are usually made on a monthly basis, but can also be made on a quarterly or yearly basis, based on the loan agreement.

Related AccountingTools Courses

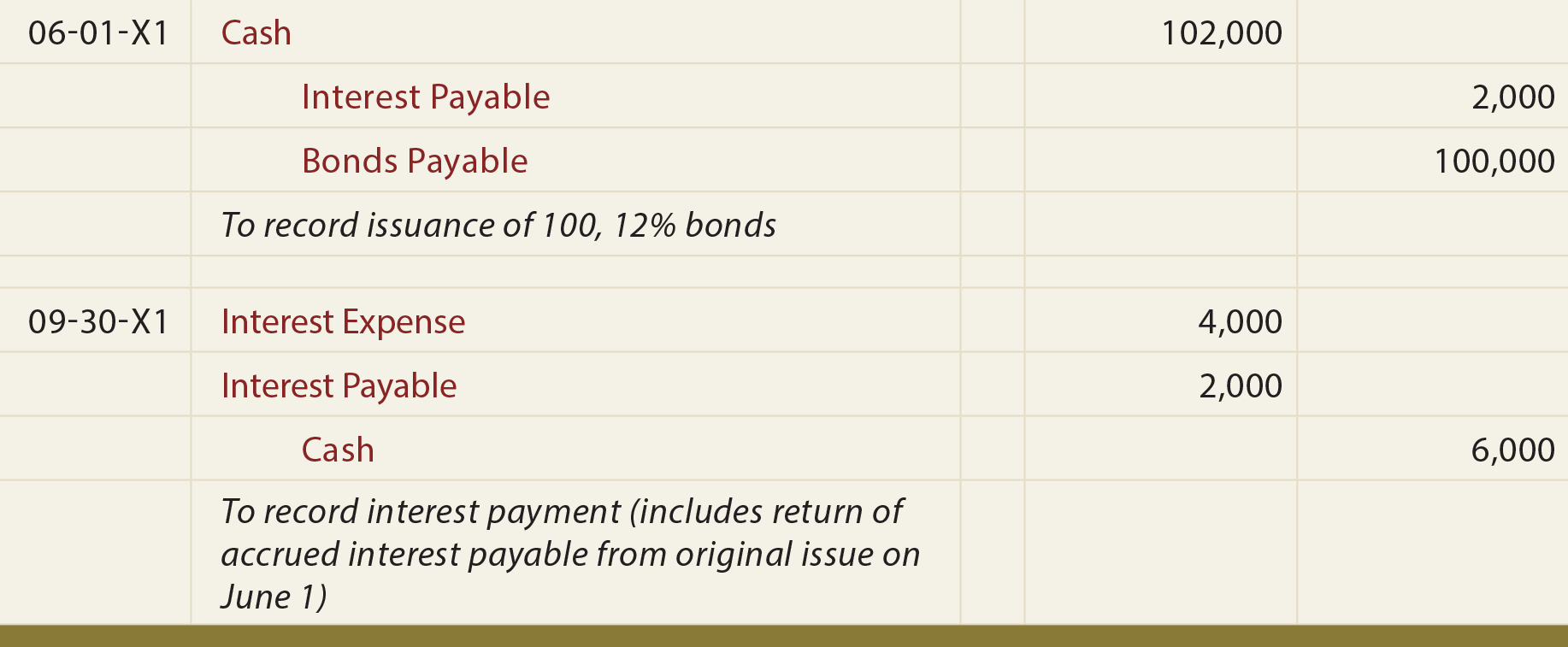

Let’s assume that the company borrowed the $5,000 on December 1 and agrees to make the first interest payment on March 1. If the loan specifies an annual interest rate of 6%, the loan will cost the company interest of $300 per year or $25 per month. On the December income statement the company must report one month of interest expense of $25. On the December 31 balance sheet the company must report that it owes $25 as of December 31 for interest. Interest Payable is a liability account that reports the amount of interest the company owes as of the balance sheet date. Accountants realize that if a company has a balance in Notes Payable, the company should be reporting some amount in Interest Expense and in Interest Payable.

What is Accounts Payable? Definition, Recognition, and Measurement, Recording, Example

Accounting rules require that all unpaid interest is recorded on the credit side of the journal entry. This helps ensure that all unpaid amounts are accounted for and that the company can accurately track its financial obligations. The current period’s unpaid interest expense that contributes to the interest payable liability is reported in income statement. Interest is not reported under operating expenses section of income statement because it is a charge for borrowed funds (i.e., a financial expense), not an operating expense. It is usually presented in “non-operating or other items section” which typically comes below the operating income.

How to Calculate Interest Expense

Interest payable is an entity’s debt or lease related interest expense which has not been paid to the lender or lessor as on balance sheet date. The term is applicable to the unpaid interest expense up to the balance sheet date only; any amount of interest that relates to the period after balance sheet is not made part of the interest payable. In general ledger, a liability account named as “interest payable account” is maintained and used to accumulate the amount of interest expense that has been incurred but not paid during the period. To record the accrued interest over an accounting period, debit your Interest Expense account and credit your Accrued Interest Payable account.

- Interest payable can include both billed and accrued interest, though (if material) accrued interest may appear in a separate “accrued interest liability” account on the balance sheet.

- Therefore, at December 31 the amount of services due to the customer is $500.

- Likewise, the accrued interest expense journal entry will increase the total expenses on the balance sheet and total liabilities on the income statement.

How to Record Accrued Interest in Your Books

Interest payable is often recorded on a quarterly or annual basis, depending on the terms of the loan agreement. You pay accrued interest because most debt obligations have an interest rate for borrowing money. When you borrow money for a house or car, you will pay interest on that amount. The interest that accrues is the amount you owe, usually at the end of the month, which is included in your loan payment. Accrual accounting recognizes revenue when it is earned and expenses when they are incurred.

It is important to carefully compare the interest rates offered by different lenders before taking a loan. By understanding the components of interest payable, businesses can ensure that they are accurately accounting for and paying their creditors. Furthermore, businesses can use the information to inform their financial decisions and ensure that they are making wise investments.

The $13,420 of Wages Expense is the total of the wages used by the company through December 31. The Wages Payable amount will be carried forward to the next accounting year. The Wages Expense amount will be zeroed out so that the next accounting year begins with a $0 balance. what you need to know about your 2020 taxes And also, the interest expense that needs to be paid after December 31st won’t be considered, as we discussed earlier. Now, since the loan was taken on 1st August 2017, the interest expense that would come in the income statement of the year 2017 would be for five months.